Synopsis

A/R Agining more than 45 days outstanding < A/R Agining less than 45 days outstanding

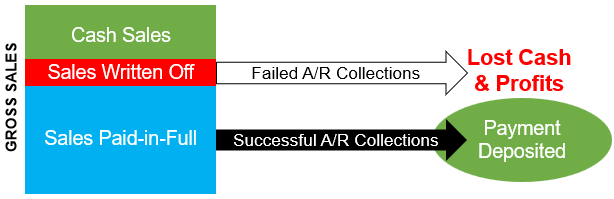

Collecting monies owed when they are due for work performed is at the heart of protecting the velocity of your cash flow. If you are a cash-only business that requires deposits made on all purchases and does not extend credit terms, you will have optimum cash velocity because you collect some of the money before work begins on a sale and the balance upon delivery.

If you are a business that extends payment terms, then the velocity of your cash flow is determined by how well you manage the collection of the monies owed to you as reported in your Accounts Receivable (A/R). A/R is reported on the Balance Sheet representing sales revenue from your P&L Statement waiting to be converted into cash. A/R is a current asset reflecting cash that is owed you that doesn’t become cash you can use to fund your business operations until you collect it.

Any time you extend payment terms to a customer, you have extended a business loan to your customer to purchase from you. For many businesses financing your customers is a required cost of business should you want that customer to buy from you. The problem for most small business owners is they fail to dial up their collection efforts with their past due customers like their bank does with them when their bank loan payments are late.

Anytime your customer’s A/R days outstanding balance exceeds your mutually agreed to payment terms, you are slowing your cash velocity. Allow them to be greater than 45-days past due, and you will have cash flow problems. Allow them to never pay you for what you sold them, and you will have zero cash velocity on that sale.

It is good business to act more like any lending institution when collecting the money owed to you. When you extend financing to your customers, you now have a financial services arm to the product manufacturing and or service delivery you do. Hoping you will get paid someday whenever your customers are late in paying you is not good business. Neither is allowing your company to be your customer’s long-term bank by allowing them to hold onto your money because you don’t take disciplined action to collect your money.

Business owners who are smart with cash have an A/R collection process to ensure they get paid on time. They manage their collection process to ensure a timely and systematic follow-up on the monies owed, so they collect it when there is money for the work they have performed. Your cash only helps you when it’s available to use. Allowing your customers to hold onto your cash because you are afraid to trouble them for your money leads to avoidable business problems.

You fail your business, employees, and customers when you fail to collect the monies owed you when owed.

Poor follow-through on A/R collections wipes out excellent performance by your people from sales to invoice submittal. Failure to collect the monies owed to you when due adds to all costs incurred and must be accounted for if you intend to structure the absorption of payment delays in your business model.

Statistics show that the older an account becomes, the higher the risk of not collecting. Research has shown that 30 days past due customers, only 99 cents out of every dollar will be collected. Beyond 30 days past due, the chances of collecting become progressively poorer. At four months, this reaches 50 percent and continues to drop with time.

Consider a company with one million dollars in accounts receivables. For every day that company delays collecting money from their customers, they need the equivalent of a $2,740 loan per day ($1,000,000/365) to cover the cash they don’t have access to in their bank account because it is sitting in their customer’s bank account.

What if your company had, and you allowed your customers to go from paying on time at 30 days to paying in 60 days. I.e., 30 days late because no one kept track of them means you would need an $82,192 bank loan ($1,000,000/365*30) to cover them for not paying as agreed.

Your A/R collections process is how you collect the money owed to you by your customers per the terms of the contract as established at the time of the sale and restated on the invoice. You reduce the need for external working capital financing by being more disciplined and deliberate in collecting the monies owed to you for work completed based on the agreement entered into before any work was begun.

Do you have high or low-risk accounts receivable?

Click here to confirm how critical your A/R collections problem is through a “free” assessment by a certified BusinessCPR™ Business Scientist. Within twelve hours of receipt of your current A/R Aging and Balance Sheet reports you will receive back by email your free A/R collections risk assessment profile.

Do you have high or low-risk accounts receivable?

Click the link below to confirm how critical your A/R collections problem is through a “free” assessment by a certified BusinessCPR™ Business Scientist. Within twelve hours of receipt of your current A/R Aging and Balance Sheet reports you will receive back by email your free A/R collections risk assessment profile.

FREE ASSESSMENT