Synopsis

Business owners who use their financial statements to help them make informed business decisions refuse to manage their businesses blindly. They know it’s essential for their business to have in place day-to-day routines that enable them to have accurate and timely financial records that give them direct insight into where their business is doing well and where it is underperforming or failing.

Your confidence in developing an achievable twenty-four-month profit plan starts with the quality of your historical financial data. Successful and Significant profit stage business owners understand the importance of keeping accurate, organized, and timely financial records. They know that having an accurate transaction recording system is the only way to effectively and efficiently manage their business activities.

Don’t underestimate the importance of accurate financial records.

Without the financial details that accurately confirm whether they are making or losing money, they would never know if they own a succeeding or failing business. Business owners who regularly work with their financial statements, not just at tax time, are refusing to operate their businesses blindly. Instead, they know it’s essential to their business to have in place day-to-day routines that enable them to have accurate and timely financial records.

These business owners use accounting software like QuickBooks or Sage to know if their customers have paid them, to track their expenses, and to keep track of who the business owes money. They use the reports generated from their financial information management system (FIMS) to build their profit plan. And then, they use these same reports to track their actual-to-planned performance.

Your chart of accounts is the foundation for creating financial reports you can trust.

The backbone for accounting accuracy is the Chart of Accounts or COA. It forms the underlying foundation that allows you to record and track your company’s financial progress. Smart business owners maintain an accurate COA as part of their habit of accurate + timely record-keeping.

These financial statements give them direct insight into where their business is doing well and where it is underperforming or failing. They know a poorly designed COA results in misleading information, leading to poor decisions and, in turn, undesirable results. The most common error from a misaligned COA is understating the cost of goods sold (COGS) by overstating the selling, general, and administrative expenses (SG&A). This situation occurs anytime a COGS account is listed with SG&A items in the chart of accounts.

Why is this a problem? When you understate your COGS, you incorrectly inflate Gross Profit. This leads to an inaccurate belief that you are pricing your products and services correctly because “look at all that gross profit being produced.” Creating the most common reason why people get confused about the difference in profits being reported through their P&L Statement and what’s shown on their bank statement.

The reality is you aren’t making the money you think you are on each sale, particularly when you fail to factor in an accurate overhead absorption. The result is less cash being generated to cover your nonoperating expenses, which leads to less cash in the bank. The solution is to always place your variable and fixed expenses in their proper chart of accounts categories.

Every COA is the equivalent of using a five-drawer filing cabinet to store all your different business transactions. Each drawer represents a different account type created within the COA as virtual “folders” that fit into one of the following five drawers.

- Assets—These are the items your business has in its possession: monies in your bank accounts, inventory that you have on-hand, and equipment used in your operations.

- Liabilities—These include monies that your business owes to others: an auto loan on a car you use for business, a mortgage that you carry on your warehouse, or sales tax you’ve collected from your customers and that has not yet been paid to the state.

- Owner’s Equity—Equity is everything your business owns: any money an owner invests in their business is considered equity.

- Income—Income is the proceeds from the sale of products or services. For example, plumbing services sold or the sale of five lamps to a customer is considered income. Nonoperating income such as interest income, tax refunds, insurance settlements, and the like involve monies coming into the business that is not generated by your normal operations.

- Expenses—This is your largest drawer organized into direct, variable, and other expenses.

- Cost of Goods Sold—These are what you purchase to complete an order, such as direct labor, materials, and equipment used to produce goods or services that are then invoiced to your customers.

- Expenses—These are items that you pay to run your day-to-day business operations. For example, advertising expenses, office payroll, insurance, and office supplies are all categorized as expenses.

- Other Expenses—Transactions kept in the back of the expense drawer involve all nonoperating expenses. Here you will find extraordinary expenses, interest expense, taxes, depreciation, and amortization expenses.

According to Generally Accepted Accounting Principles (GAAP), the standard order for assigning account numbers within the Chart of Accounts is as follows. Smart business owners use this same logic to better ensure they have accurate and consistent financial reporting.

1000 – 1999 Asset Accounts Things you own

2000 – 2999 Liability Accounts Things you owe

3000 – 3999 Equity Accounts Your investment in your company

4000 – 4999 Income Accounts Is the revenue you earn

5000 – 5999 Cost of Sales Accounts Are the direct costs you pay

6000 – 8999 Overhead (SG&A) Expenses Are the indirect costs you pay

9000 – 9999 Other Revenues/Expenses Non-operating, extraordinary

Net Profit [Loss] What’s left offer after all accounting

Below is a visual of your chart of accounts, including a reference to the recommended account numbering per the generally accepted accounting principles known as GAAP reporting:

Profitable businesses have day-to-day routines they follow to have accurate and timely financial records that give them direct insight into where their business is doing well and where it is underperforming or failing.

What if I know my financial statements aren’t accurate?

If you have doubts about the accuracy of your historical P&L Statements, you should hold off building your profit plan until you have improved the accuracy of your chart of accounts. The good news is once you have a properly aligned P&L, a quality accounting software program will easily allow you to access both forward-looking and retroactive data that reflects the changes you make.

This means that all future transaction recordings use the new account structure. Your financial system will also transfer historical data into the new COA format. In other words, you won’t have to “restate” historical Balance Sheets or Income Statements to make them consistent with future reporting. This huge time-saver helps ensure that your historical data will be reflected accurately, allowing comparisons to be made more easily.

Once you are confident that you have your variable and fixed cost transactions properly mapped to their correct COA expense category, you can proceed with building your profit plan.

Without accurate + timely financial reports, you never know what financial information you can and can’t trust.

In completing BusinessCPR™ Step 2, you will have invested considerable time and effort to confirm that your financial statements are accurate and “make sense” to you. These monthly statements, for the last forty-eight months would have been analyzed and used as inputs into setting your twenty-four-month profit plan.

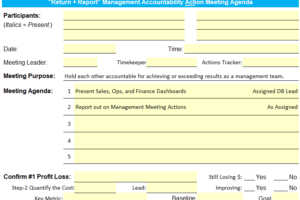

BusinessCPR™ Step 3 confirms the quality of your profits-to-plan results through a disciplined review of your monthly financial statements. This review is anchored by your monthly P&L Statement, where you learn, each month, whether you are making the intended profits or suffering losses. Your review of your P&L results by month is how you ensure that your business is on track to achieve its expected profits as well as its revenue targets and expense budgets.

Failure to review your financial statements every month means you never know whether your cash flow, profits, or owner’s equity are increasing or shrinking month-to-month.

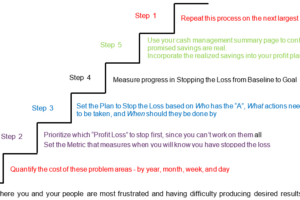

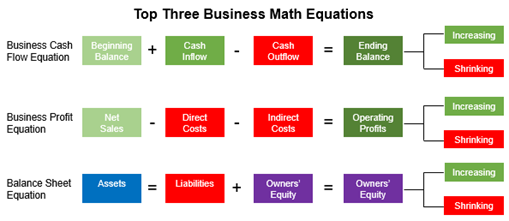

Use the Math of Business to manage the relationship across Cash flow, Profits, and Reporting to stop being cash-poor.

Your financial statements provide you with one of the easiest-to-use business management tools that exist.

One of the most accessible keys to success available to every business owner is the power to make smarter decisions through the month-to-month use of their financial statements. Business owners and management teams benefit significantly through the consistent monitoring of these critical reports on the performance of their company.

You must record your transactions accurately and promptly to ensure that the decisions you’re making and the actions you’re taking are producing the desired results month to month. The key to you having more cash in the bank is in how this information better positions you to eliminate unnecessary profit losses. If you are failing to reach any one of these lagging indicator goals for a given month, you have identified a specific area for considering corrective action.

As you identify what corrective action needs to be taken, think about who is responsible for accomplishing it and when it needs to be completed—being clear on the who, what, and when associated with each corrective action is essential to avoid falling short of your goal. Remember, over time, each repeat lagging metrics miss, if not corrected, will also cause you to miss your monthly, and ultimately, your annual profit goals.

Are your financial statements accurate?

If you want financial statements you can trust, then you need a properly aligned chart of accounts. Click here for a “free” assessment of your chart of accounts from a certified BusinessCPR™ Business Scientist who will review your P&L Statement and Balance Sheet to see what they reveal about your chart of accounts.

Within two days of receipt of the multi-year P&L Statement and Balance Sheet, you will receive an email with your free chart of account review.

Do you trust your financial statements?

Are your financial statements accurate? Do you trust them? If the answer is no, click the link below for a “free” assessment of your chart of accounts from a certified BusinessCPR™ Business Scientist who will review your P&L Statement and Balance Sheet to see what they reveal about your chart of accounts.Within two days of receipt of the multi-year P&L Statement and Balance Sheet, you will receive an email with your free chart of account review.

FREE ASSESSMENT