Synopsis

If you have been doing the same thing over and over and are getting worse and worse results, then developing a strategy is a “nice to do.” The “must-do” is profit planning that defines the set of targeted actions you plan to take across sales, operations, and finance to achieve your profit goals. Rather than set arbitrary profit strategy targets for sales, gross profit, and operating income, it’s better to appreciate your business’s performance over the last four years by month. This is particularly true when you aren’t in a rapidly changing industry where it’s hard to anticipate customer demand.

Most strategy experts believe past performance is not a good indicator of future results. They believe that the conditions that led to that past performance will have changed in some way and are irrelevant. This is particularly true if you are in a rapidly changing industry like high technology, where a new development can make what you sold last year obsolete this year.

If you are in a rapidly changing industry where it is often hard to anticipate customer demand, then developing your strategic plan is a mandatory precursor to building your profit plan.

If you have been doing the same thing repeatedly and are getting worse and worse results, then developing a strategy is a “nice to do,” not a “must do.” Even if you have decided to make significant product changes, having a new and accurate profit plan that reflects those changes is the “must-have” for the next year. You focus here because profit planning defines the set of targeted actions you plan to take across sales, operations, and finance to achieve your profit goals.

Rather than set arbitrary profit targets for sales, gross profit, and operating income, it is advised to first review and appreciate your business’s performance over the last four years by month.

Should I use accrual or cash basis accounting to assess the results of my past performance?

Accrual accounting matches accomplishment (delivery of product or service) and effort (expenses incurred to generate accomplishments) regardless of cash-flow timing. This is the preferred accounting method for profit planning because it most closely correlates the timing of the revenue to the expense.

Cash accounting is the simplest of the two primary accounting methods to perform. Put simply, this method records income when cash is received and expenses when cash is paid out. What’s interesting is how many accountants advise small businesses to adopt cash accounting for tracking their tax liability, a method that is not considered a useful management tool. It leaves a time gap between the recording of the cause of action (sale or purchase) and its result (payment or receipt of money).

The generally accepted accounting principles (GAAP) accountants use to prepare financial statements is accrual basis accounting. With this method, expenses are reported when goods or services are entirely consumed, regardless of when the bill got paid. Likewise, revenues are reported when the product or service has been delivered, creating the right to receive a cash payment, regardless of when the business gets paid by the customer.

In building a profit plan, it is best to use accrual basis historical financial statements because this accounting method better matches the timing of revenues and expenses. If you are unsure of the payout timing for any particular expense, particularly your SG&A expenses, it is advisable to look at your P&L Statement by month on a cash basis.

Start your profit plan with at least your last thirty-six months of P&L reporting.

The most efficient way to build your profit plan is to start with a download of your previous thirty-six to forty-eight months of P&L results. Only take this step after determining that your historical P&L statements are an accurate reflection of your management’s performance. If you are unsure about why this matters, click here to read, “Why is the accuracy of business financial records vital to every business owner.”

P&L Statement accuracy is the key to building a realistic Profit Plan derived from the previous year’s results in setting this year’s targets. Your historical P&L Statement itemizes revenues and expenses of the past that led to your current profit or loss. As you review the results for the previous years by month, you will get an idea of what needs to be done differently or started to improve your results.

If your financial system of record is QuickBooks, you can use the following guide to export a forty-eight-month view of your income statement from QuickBooks into a Microsoft Excel file:

Begin planning for profits with insights you gain from analyzing your historical results by month.

Following this data download, your goal is to begin your profit planning with your historical insights. It’s essential to review them first to identify what needs to be done differently to produce higher profits. The easiest way to do this is to group your historical P&L line items by month into the following buckets for ease in building your profit plan:

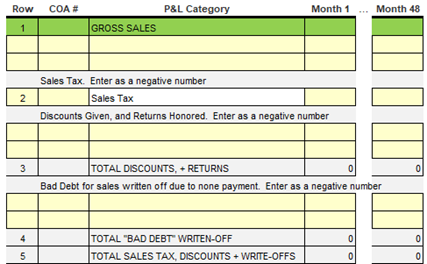

Gross Sales or Revenue or Income – this is your Top-Line

Net Sales or Revenue or Income – this is what you collected from your gross sales after you subtract from Gross Sales the sales tax to be paid, discounts given, returns honored, and bad debt for sales written off due to non-payment. Your Net Sales reflect the sales you received payment for representing your operating cash inflow.

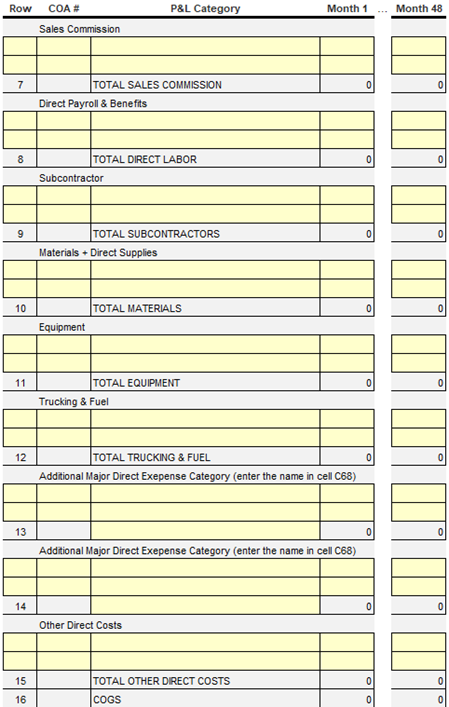

Direct Operating Costs or Variable Costs or Cost of Goods Sold or COGS reflect those costs incurred to produce the product or service that your customers paid you to deliver and perform for them.

What is left over after paying your direct costs tied to delivering on your sales commitments is your first measure of profitability and is the most vital number in your business.

Indirect Operating Costs or Fixed Costs or Overhead or Selling, General & Administrative Expenses represent those expenses in your business that do not vary with how much you sell.

What is left over after paying for every fixed and overhead expense tied to your business is an excellent measure of how efficient you are in managing your business.

Non-Operating Income, Costs, and Expenses such as Owners Compensation, Other Income, Other, One-time, or Extraordinary Expenses then Interest, Taxes, Depreciation, and Amortization are all nonoperating numbers that need to be accounted and planned for outside of your normal business operations.

What is left over after paying for every expense tied to your business during any accounting period is your Net Profit. This is the only number that transfers over to your Balance Sheet.

Once you have pulled your historical data together, you can now begin to identify what needs to be done differently to make more money. Analyzing your P&L financial results is easier when it is in a consistent format, like what’s represented above. Knowing what’s worked well in your business, where you lost money, and what you want to do differently is how you position yourself to set realistic profit plan targets by product, cost of goods sold, and selling, general, and administrative expenses.

Would you like a free tool to help plan for profits?

Click here to download the Excel template to organize your P&L historical data. Using this template will help you more efficiently review the results for the previous years by month. As you do this, you will get an idea of what needs to start, stop, and be done differently in your business to improve your profitability.

Would you like a free tool to help plan for profits?

Click the link below to download the Excel template to organize your P&L historical data. Using this template will help you more efficiently review the results for the previous years by month. As you do this, you will get an idea of what needs to start, stop, and be done differently in your business to improve your profitability.

READ THE TIPS