Synopsis

You position yourself to make more money when applying both microeconomic theories for opportunity costs and the law of supply and demand to how you price your products and services. Do this to understand better how demand for what you do has a significant effect on your ability to earn a profit.

The discipline of economics represents the theories, principles, and models that deal with how the market establishes the value for work. Economics attempts to explain how wealth is created and distributed in communities, how people allocate scarce resources, and issues dealing with human wants and satisfaction.

The problem with applying micro or macroeconomics teachings to owning a profitable business with predictable cash flowing through it and reserves in the bank is that economics is more academic than practical. The two most practical theories from microeconomics are opportunity costs and the law of supply and demand, two of the most important concepts we learn in economics.

Understanding both economic theories matters to every business because price affects demand. Higher prices decrease the demand for any product or service. When the price of an item or service is high, individuals must consider that buying the item may prevent them from purchasing another, more valuable item. As a result, the opportunity cost of the item under consideration may be seen as too high. If this is the case, there will be less demand for that item at that price point.

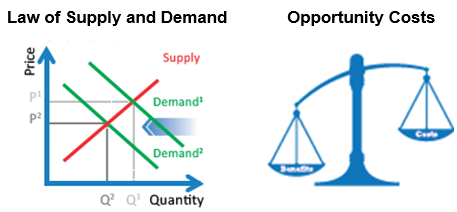

The law of supply & demand impacts everything in your business

This fundamental truth in business is furthered through the law of supply & demand. A law of business that is highly relevant yet often overlooked in understanding the power of price, value, and profits.

In 1767, in The Wealth of Nations by Adam Smith identified how the unit price for a particular good varies until it settles at a point where the quantity demanded by consumers approximately equals the quantity supplied by producers at a particular price, which results in an economic equilibrium for price and quantity.

What makes knowing the theory of economic equilibrium a “so what” for small businesses is that no marketplace ever achieves economic equilibrium. Yes, it’s a terrific academic point to teach, but not relevant. What is relevant is knowing the recognized drivers of supply as a determiner of price and demand as a price influencer:

The four recognized drivers of supply as a determiner of price involve the following:

- The production costs: how much does the item cost to produce

- The technology used in production and its rate of advancement

- Your knowledge of and expectations about future prices

- The number of suppliers that exist in the current market

The four recognized drivers of demand as an influencer of price are:

- The income levels of those buying

- The prices of related goods and services

- The consumers’ expectations about future prices and incomes

- The number of potential customers

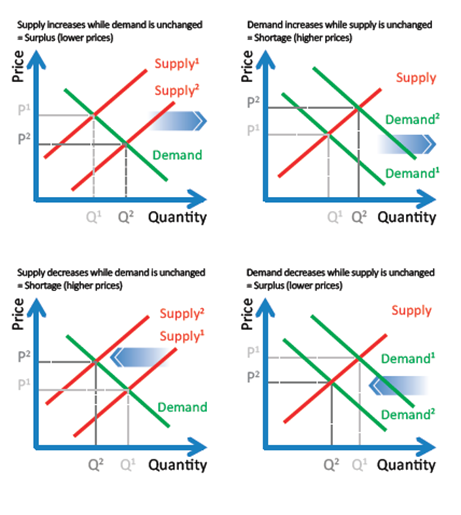

Below is a visual representation of the law of supply and demand drivers that exist when you don’t have price/quantity equilibrium. Understanding which demand and supply scenario your business competes in will help you better understand what pricing your business situation will allow you to charge:

As shown above, if supply is tight for your particular product and demand is high for similar products, you will have the opportunity to earn higher profits. Unfortunately, you’ll also face the risk of new competitors entering the attractive market. Even more unfortunate is how rare it is to compete in this type of market.

When supply is high and demand is low, you will find yourself engaged in a price battle. Most businesses operate in this type of market, in which the winners are often those with the lowest costs of production.

The economic theory of opportunity costs impacts how time and money get spent with your business and by you.

In economic terms, “opportunity cost” is what a person sacrifices in choosing one option over another. Opportunity costs are defined as the value of the “next best alternative.” The item that you don’t choose is the opportunity cost. It is a measure of the sacrifice we make when we are forced to make choices.

For your customers, the value of your product is primarily shaped by their perception of the price they will pay and the benefits they anticipate from their purchase. Those who think like economists on large purchases will also include other things that they must be willing to give up to buy from you in deciding to buy or not.

The other part of economic opportunity costs is that price affects demand. Higher prices decrease the demand for any product or service. When the price of an item or service is high, individuals must consider that buying the item may prevent them from purchasing another, more valuable item. As a result, the opportunity cost of the item under consideration may be seen as too high. And this will result in less demand for that item at that price point.

For example, in addition to paying cash, a customer may have to spend time learning to use a product, pay to have an old product removed from their home or office, or temporarily close down their current operations while a product is being installed; or they might have to incur other expenses. Beyond the actual price they pay for the transfer of ownership, these additional costs can be very real or seen as opportunity costs.

Opportunity costs impact not only your customers’ decision to buy from you. It also consciously and unconsciously impact how you spend your time and money. In the day-to-day operation of a business, opportunity costs are best seen when cash flow is tight. Particularly as it relates to taking the “do it yourself” approach to getting things done. Those who take this approach versus paying someone else to do it for them occur when they see themselves with the time, skill, but not the money.

The challenge with doing in yourself is the too frequent underestimation of the time and skill level required to do it yourself, successfully. More often than not, small business do it yourselfers spend more money “doing it myself” than they would have paid a professional to do the work.

What gets missed in deciding whether to do it myself, don’t do it, or pay someone else to do it is the economic theory of opportunity costs. Opportunity costs are about tradeoffs involving the currency of business. Every day you and those who buy from you are trading time or money to acquire what they need and want. The best way to make this decision is to establish the price/value equation for big-ticket items to the item being considered and the next best alternative. Being able to calculate the difference between what you have to pay to acquire it and the anticipated value to be received is how you know what your best path forward is relative to doing it, not doing it, or paying someone else to get it done.

The price you charge for your products and services has a significant impact on the demand for what you do and the amount of profits you are likely to earn on each sale. You better position your business model to make you more money by applying the principle of opportunity costs, the law of supply and demand, and the 7-P Framework to what you do. Using the knowledge you derive through these insights is how you better ensure you have a profitable business model.

Are you violating proven economic theory?

Click here to have a certified BusinessCPR™ Business Scientist confirm what your financial statements tell about how well your business applies the principle of opportunity cost and the law of supply and demand to your business. Within forty-eight hours of receipt of your P&L Statement and Balance Sheet by year, you will receive back by email your free assessment of what your financials tell you about the economics of your business.

Are you violating proven economic theory?

Click the link below to have a certified BusinessCPR™ Business Scientist confirm what your financial statements tell about how well your business applies the principle of opportunity cost and the law of supply and demand to your business. Within forty-eight hours of receipt of your P&L Statement and Balance Sheet by year, you will receive back by email your free assessment of what your financials tell you about the economics of your business.

FREE ASSESSMENT