Synopsis

You increase the benefits you offer your customer each time you increase the perceived value for what they buy from you or decrease your price. Either way, you are increasing value. The decision you must make is what kind of value perception do you want to create.

There are only two viable levers to employ when it comes to price for every business. You can increase the benefits to increase the value for your customer, or you can decrease your price. Either way, you are increasing value, as shown below:

Deciding how best to communicate the value you offer is determined by what kind of value perception you want to create in the mind of your target customer. If your goal is to use a lower price to create value for your customer, the marketing lever is place. Anytime you lower the price, you are making it easier to buy.

If you want to hold your price or charge a premium price for the value you offer, your marketing lever is promotion. Here your goal is to promote greater value through better benefits.

If your target customer tells you that you are too expensive, you have failed to communicate the benefits effectively or compete against a more operationally efficient business. This does not dismiss the reality that some people are only happy when negotiating a deal. When that happens, ask them, “What do you think is a fair price for the value I am giving you?”

If you think their price counter is fair. One that leaves you an acceptable amount of profit for the risk, costs, and efforts you have to make, then take it. Accepting fair price counters takes price out of the sales presentation allowing you to move the sales prospect on to the what, when, and where considerations.

If you don’t think that their counter price is fair, you still need to move the sales prospect on to the what, when, and where considerations of what you are offering. The only difference is now you are looking to identify what you can take away from your product or how they acquire and use it to reduce your costs so you can reduce your price and still earn the profit you deserve.

The key to making more money is to earn the right to increase your price by clearly providing greater benefits to your customers, so they will prefer to bring their business to you. You do this when you provide more of what your customer wants without a substantial increase in delivery cost. The best way to do this is to solve an irritation or remove a potential fear.

As your customer approaches the decision to buy from you, any fear or insecurity that arises makes it harder for them to connect to the value you are creating for them. This fear dissipates when they gain confidence in your company and believe that your solution will solve their problem.

You do a lot to help your customers overcome the fear of doing business with you by creating clarity and accuracy around knowing who they are, what they need, when they need it, and where they will find it.

The team you employ and pay are the ones that drive your costs and create the value you offer

You make superior value connections with your customers when your employees understand the why and your customers see how your business is unique. Providing clear answers to these questions allows you to set, and maintain, a price for your products and services that provides a good value to the customer and a profit for you.

No one wants to incur a cost higher than the benefit they derive. When establishing the prices you charge, you avoid being seen as a poor value by either increasing benefits or decreasing costs to increase perceived or real value to the customer. When you know what people perceive as value, and your employees understand how to deliver that value cost-effectively, you will earn higher profits.

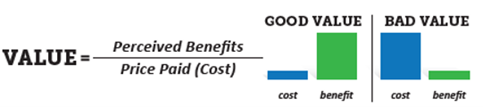

The customer price/value equation is more than just the price you charge

Below is a simple illustration of the customer PRICE/VALUE equation that lies at the heart of the majority of purchase decisions made every day:

The value of a product for any buyer centers on their perception of the price they will pay relative to the benefits they expect to receive from their purchase. The price paid in a transaction is not only financial. It may involve other things that a buyer must be willing to give up.

For example, a customer may have any combination of factors in addition to paying cash for your product or services:

- Spend time learning to use the product,

- Pay to have an old product removed from their home or office, or

- Temporarily close down their current operations while a product is being installed,

- Incur other expenses to install the product or work with the service.

Beyond the actual price a customer pays for the transfer of ownership, these additional costs can be real, or they can be seen as “opportunity costs.” In economic terms, “opportunity cost” is what a person sacrifices in choosing one option over another. The item that you don’t choose is the opportunity cost. It is a measure of the sacrifice we make when we are forced to make choices.

Should I lower costs or increase value to make more money?

Click here to learn if the secret to increasing your profits lies in lowering costs or increasing value. Within thirty-six hours of receipt of your P&L Statement and Balance Sheet by month, you will receive your free answer from a certified BusinessCPR™ Business Scientist to which price lever makes the most sense for your business by email.

Should I lower costs or increase value to make more money?

Click the link below to learn if the secret to increasing your profits lies in lowering costs or increasing value. Within thirty-six hours of receipt of your P&L Statement and Balance Sheet by month, you will receive your free answer from a certified BusinessCPR™ Business Scientist to which price lever makes the most sense for your business by email.

GET THE ANSWER