From an accounting perspective, the biggest challenge with Interest Expenses involves fully accounting for the Interest Expense you pay each month. Keeping a record of the interest expenses you incur and pay is a tax-deductible cost of doing business that too many fail to account for accurately.

The bigger challenge with Interest Expense is it represents never-ending Cash Outflow until the borrowed money being charge interest is paid off. All is well as long as the borrowed money earns a greater return represented by Cash Inflow each month than the principle and interest payments being Cash Outflowed.

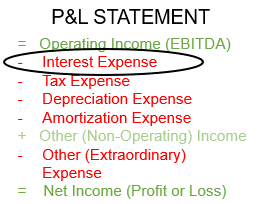

Overview

Interest Expense is the cost of money a company pays for borrowing from a bank or other lending institution to buy an asset or pay down a high-cost liability of any kind. For example, when you buy a piece of equipment using a bank loan, you must pay not only the amount you borrowed, you must also pay the agreed-upon interest based on the interest rate being charged on the amount you borrowed.

It is the interest paid, not the principal amount, that is included in this nonoperating expense. Including interest expense within SG&A Expenses understates Operating Income and the impact of overhead expenses. It is to be treated along with Nonoperating Expenses as part of Earnings Before Interest, Taxes, Depreciation, and Amortization or EBITDA.

Again, accounting for Interest Expenses accurately helps you have confidence in the accuracy of your P&L Statement. The bigger issue is the impact of monthly principle and interest payments on your cash flow. Struggle to have sufficient cash to cover your debt obligations and it won’t matter how well you account for your interest expenses.