Do you have significant nonoperating expenses that, if not incurred, would negatively impact your ability to operate your business? If yes, treating them as “extraordinary costs” either misrepresents Gross Profit or Operating Income. It is impossible to control expenses if you aren’t recording the associated expense transactions where they belong.

Overview

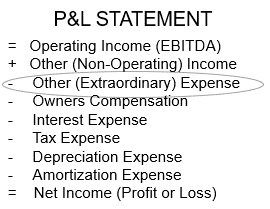

Other Nonoperating Expenses, often referred to as extraordinary expenses, are those not directly attributable to the company’s core business operations. Any nonoperating or extraordinary (one-time) expenses that are considered unusual, infrequent, and not attributable to business operations should be reflected here and not reflected in COGS or SG&A. You account for these expenses here because the owner incurs them as part of owning the business and aren’t a part of ongoing operating costs.

Another test on the significance of Nonoperating Expenses to Net Income and Cash Reserves is whether a 10% reduction in this general ledger account would have a significant change your Net Income dollars? If yes, what are you going to do about it, and who is accountable for getting it done?