Should you seek outside financing, know that creditors will use Liquidity Ratios to measure your ability to meet your short-term obligations.

The results of their calculations will tell them how well you could turn liquid assets into cash to pay off liabilities and other current obligations. You will have difficulty securing outside financing if they see Current Liabilities close to Current Assets.

Overview

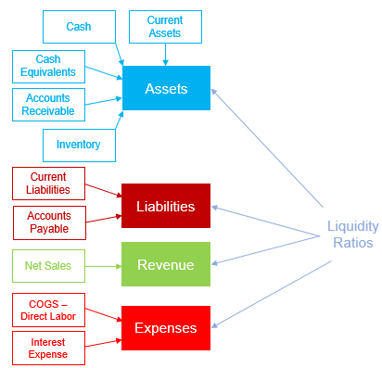

Liquidity measures a company’s ability to meet its near-term financial obligations through liquid assets that can be quickly converted to cash. These assets are reported on the Balance Sheet as cash, short-term investments, current A/R, and inventory.

Liquidity Ratios are the second most widely used ratios, coming in at a close second to Profitability Ratios. Creditors use Liquidity Ratios to measure a firm’s ability to meet its short-term obligations by turning liquid assets into cash to pay off liabilities and other current obligations. The most common Liquidity Ratios are the following:

- Working Capital or Current Ratio

- Quick Ratio

- Cash Ratio

- Accounts Payable Turnover

- Times Interest Earned Ratio

The above ratios measure how easy it will be for the company to raise enough cash or convert assets into cash to pay off its Current Liabilities as they become due, as well as its long-term liabilities as they become current.