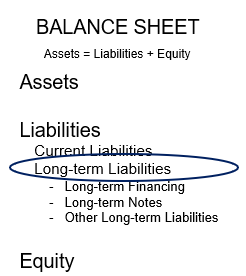

If your Long-term Liabilities are higher than your Fixed Assets after Depreciation, you owe more than your core assets are worth.

Either get your assets to earn you higher profits so you can pay down your debt or sell off underutilized assets to free up cash to pay down your Long-term Liabilities. For most businesses in this situation, doing both is the best approach.

Overview

Long-term Liabilities are financial obligations or debts incurred during business operations that are payable over a period greater than one year from the date of the Balance Sheet.

Long-term debt restricts your monthly cash flow in the near term. The higher your debt balances, the more you have committed to paying on them each month. This means you must use more of your monthly earnings to repay debt rather than encourage new investments to grow. It also limits your ability to build up a safety net of cash reserves to cover unexpected business costs.

The other challenge with long-term debt is tied to collateral. Using personal and business assets as security to gain financing at reasonable interest rates puts you at risk of losing the asset through repossession if you get into a cash flow crisis and fall behind in your payments.

What’s worse is taking on Long-term Liabilities that fail to earn a return on the debt-financed asset with a personal guarantee. Agreeing to provide a personal guarantee means that the individual assumes personal responsibility for the balance if the business cannot repay the debt. Should this happen, the creditor will go after personal assets such as your home if your business fails to repay the loan.

If you are not 100% sure of the profits to earn from this highly risky payment guarantee, think twice as hard about making the asset purchase until your business is stable enough to qualify for financing without you guaranteeing the debt.