Operational inefficiencies show up in a declining Operating Margin Ratio caused by anything from nonproductive labor to wasted materials to paying too much for any expense will leave a company at a cost disadvantage.

Fail to eliminate the inefficiency, and you will either have to increase your prices to make a profit or be driven out of business by your competition, which doesn’t waste money.

Overview

Operating Margin Ratio is a Profitability Ratio representing what’s leftover from a dollar of sales after subtracting all costs associated with producing, acquiring, and selling your products and services. It calculates what is available from each dollar of sales to pay the company’s fixed expenses, capital providers, and its taxes after subtracting depreciation and amortization from Net Sales.

The Operating Margin Ratio is the best measure of operations managerial performance relative to how much revenue is left over after all operating costs have been paid. This number reveals what proportion of revenues is available to cover non-operating costs.

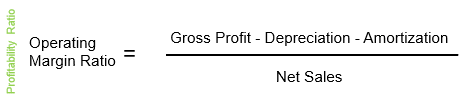

The formula for Operating Margin Ratio is as follows:

(Gross Profit – Depreciation – Amortization) / Net Sales

A 20% Operating Margin Ratio means that for every dollar of sales, only 20 cents remain to cover the non-operating expenses of a business before a profit can be realized.

Higher is Better: the more money from operations to pay for its fixed costs, the more stable the company.

Lower is Worse: using non-operating income to cover operating expenses shows that operating activities are not sustainable.