Retained Earnings is the most telling Balance Sheet number of management effectiveness in converting sales into profits. It represents the “sum of all profits” retained since the company’s inception, less reported losses.

Overview

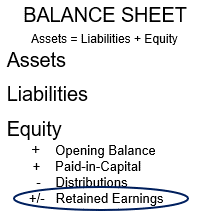

Retained Earnings represent the profits a company has earned as of the date of the Balance Sheet, less any dividends or other distributions paid to investors. This amount is adjusted whenever an entry to the accounting records impacts a revenue or expense account.

Mathematically, it is the accumulated undistributed earnings of a company retained for future needs or for future distribution to its owners from profits generated by a company that is not distributed to stockholders (owners) as dividends. Retained Earnings do not represent surplus cash. Instead, Retained Earnings demonstrate what a company did with its profits—the amount of profit it has reinvested in the business since its inception.

Retained Earnings are not an asset. They are considered a liability to the business—money that has been set aside to pay stockholders in the event of a sale or buy-out of the business. Consequently, Retained Earnings are part of stockholder’s equity. They are also referred to as accumulated earnings, accumulated profit, accumulated income, accumulated surplus, earned surplus, undistributed earnings, or undivided profits.

You impact Retained Earnings through Net Income. This bottom-line number from your Balance Sheet is the only number that transfers from the P&L Statement to your Balance Sheet. When a business fails to realize its Net Income goal, they fail to realize higher Retained Earnings. Prevent this from happening by applying the discipline of the BusinessCPR™ Management System to improve your ability to convert sales into profits that increase your owners’ equity in the business.