For most small businesses, the Product Contribution Ratio is nice to know more than a must-know.

The better measure of the profit contribution of a product is reflected in the management distraction of a product. Should management have to spend large amounts of time resolving problems with a specific product line over other products produced, that product needs to be fixed or dumped.

Overview

Gross Profit Margin is the average Gross Profit for all products and services sold. Product Contribution Margin represents the Gross Profit contribution of an individual product line or service to the business. It represents the difference between a product’s sales revenue and the variable costs allocated to that product.

The Product Contribution Margin Ratio measures how much individual product lines contribute to business profitability. Sales, Product Line, and Operations Managers use this calculation to confirm products are priced appropriately and to concentrate sales and operating procedures improvement by product line.

Big businesses know which products pay their bills and which contribute less because they track COGS by product. Small businesses can’t tell you the profit contribution by product line because they find it too difficult to allocate direct costs to specific products.

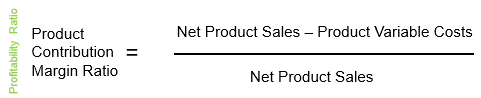

The formula for calculating the Contribution Margin Ratio is as follows:

Net Product Sales – Product Variable Costs / Net Product Sales

A 40% contribution margin per unit means that for every dollar of unit sales, 40 cents remain from that sales dollar to cover other expenses. A 25% contribution margin per unit means that product sales contribute 15 cents less for every dollar sold than the higher-margin product.

Higher is Better: products produced and sold contribute to covering other business expenses.

Lower is Worse: you should question the value of selling a product if it fails to contribute margin to cover other expenses.