An investment made in your business that generates an acceptable Rate of Return (RRR) on the sales it generates reduces both the cash pressure and risk exposure on the business.

For example, a significant investment in a business that doesn’t generate the planned sales increases will always result in greater cash pressure, risk exposure, and stress on ownership to generate higher profits to recover from the failed investment. This is why gauging a business investment’s risk before it is incurred is critical to your peace of mind and cash conversion into profits from sales.

Overview

The Required Rate of Return (RRR), or hurdle rate, is the minimum amount of profit (return) an investor is prepared to accept for their investment. It represents the minimum compensation they will accept for investment level of risk in exchange for their money.

RRR is also used to calculate how profitable a prospective business investment will likely be relative to the investment cost. In this second scenario, RRR is like the Internal Rate of Return (IRR) in that it is a projection of probable profit to be generated from an investment.

Most investors view an average annual rate of return of 10% as acceptable, more ideal as their return on long-term investments in the stock market. Remember that this is a stock market investment with multiple investors competing to buy stock, making it appear less risky. The reality is investing in stocks is risky and should be done through a disciplined approach to assessing where to and where not to invest.

Investors don’t look to invest in small businesses because they take years before any significant returns on their investment. Because of this reality, expecting investors to jump into your equity pool with their investment is slim. This is why personal and debt financing is how most small business owners jump-start their working capital.

The value of calculating the Required Rate of Return for small businesses lies in valuing significant prospective business investments. Both RRR and IRR account for the time value of money. They are used to gauge the value of one investment over another or against a minimum required return on investment.

Once personal money or debt financing is committed to a large asset purchase, it’s committed. It is like shooting a rifle with only one accessible bullet. A small business will not likely have the cash to make a second large purchase until they have repaid through returns earned to cover an investment already made. No matter how confident a small business owner is that a significant investment will generate more profits than it costs, it will always be a risk until the profits materialize.

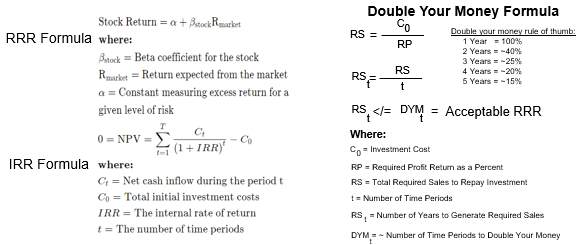

The problem with calculating either the Required or Internal Rate of Return is that neither calculation uses readily available information from your financial statements. For example, the IRR formula uses discount rates to make the Net Present Value (NPV) of all cash flows equal to zero. The problem with this complicated math is the need to know the beta coefficient, cash inflows, discount rate, initial cash outflow, and the years involved. This is why financial experts advise you to use the prebuilt Excel formulas to do this math.

An alternative method for determining the risk of an investment for a small business is to convert the cost of the investment into sales required to earn the investment back. Say an investment costs $100,000, and you want a 25% return on that investment. I.e., you have a goal of earning 25% in Net Income in your business. The sales value of that investment is $400,000 (100,000/.25=400,000). This means you will need to generate $400,000 in sales to return your $100,000 investment. The question is, how long will it take to generate the $400,000 in sales?

Use the “double your money” method to help you better determine if the proposed investment is worth the risk. For example, you want to double your money on a planned new piece of equipment in five years. To calculate what the rate of return should be on that investment, divide 100% by five to get an approximate IRR of 15% ((1/5) x 0.75) where 5 is the number of years, and 0.75 is the “double your money rule of thumb” estimate of the investment value.

Below are the most common IRR approximations you will ever need to perform the “double your money” risk component of a planned investment quick calculation:

1 Year = 100% IRR

2 Years = ~40% IRR

3 Years = ~25% IRR

4 Years = ~20% IRR

5 Years = ~15% IRR

Confirming how much you have to sell to return your investment is made easier when cross-checked against the IRR double your money rule of thumb. The above example will meet the required return in three years or less by generating $400,000 in new sales on the equipment purchase of $100,000. If new sales take four or more years to generate $400,000 the planned $100,000 piece of equipment is not the best investment for you to make.

Laying the sales value of an investment required to hit your profit goal with the “double your money” IRR approximation can help you see what an investment has to sell to earn you a planned return. Using this method to help you make a go/no go decision on an investment is driven by how fast you think you can generate the sales needed to repay the investment. Not on market forces assumptions that require higher math.

The bottom line of investment decisions is how long it will take you to earn a return on your investments. This time question is always driven by how fast you can make sales in a small business. Failure to generate the new sales the investment promises to generate will never be a return, no matter what calculation you use to gauge the risk of the investment.