Poor record-keeping means you have chosen to fly your business blind. Neglect to record your business transactions in a timely and accurate manner represents poor accounting for money coming in and going out.

Fail to know know what is going on financially in your business means you have no control over the results of your business. You can’t earn higher profits on bad numbers in your financial reports or no numbers because you don’t have any financial reports on the quality of your business results.

Overview

Effective record-keeping begins with recognizing two key factors:

First, no game is fun to play overtime when no one keeps score. Part of the fun of playing any game is knowing whether you are winning or losing (particularly when you know you are winning!) during the game.

Second, if your goal is to enjoy the long-term financial benefits of operating a well-managed business, one that runs without you, you’ll first need to learn to keep consistent and accurate financial records.

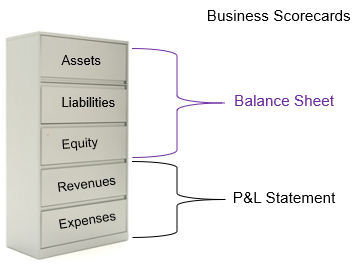

Creating an income statement or profit and loss (P&L) statement is easy. It starts with recording your revenue and expense transactions into your accounting software every week. It’s amazing how many business owners fail to record both sales and expenses incurred promptly and consistently. Too often, they’ll try to do this at the end of a month, quarter, or never at all. All because they failed to develop the habit of timely and consistent record-keeping.

As a result, they fail to record every transaction that occurs, every transaction that has one of two outcomes. Each sales transaction results in either more money coming into a business or more going out.

Successful business owners value the importance of keeping well-organized financial records. They use accounting software like QuickBooks or Sage to know if they have been paid by all of their customers. They also use accounting software to track expenses, monies owed, and payment deadlines. They do this to know whether they are making or losing money.

Struggling business owners often find record-keeping to be a difficult habit to establish. Therefore, they never practice this key routine to making a business profit and controlling cash flow. They don’t develop this discipline because they don’t understand that the “P” for profit in BusinessCPR™ comes after you have converted your sales into “C” for cash inflow and paid your expense transactions representing cash outflow and before the “R” for whether you did this at a profit or loss through your reporting.